Private equity (PE) counts on growth in 2025. Mainly more add-ons are expected.

Public-to-private deals and venture capital investments are lagging.

There is high competition in the PE market, and a lack of attractive targets.

For private equity investors, the brakes can be released in the recommended year.

By Jan Bletz

Most types of private equity activity are likely to increase in the coming months. This is evident from the M&A Trend Survey Benelux 2024 / 2025 by M&A and Ansarada. For this research, 175 Dutch and Belgian M&A professionals took part in an online survey and the M&A editors interviewed 35 dealmakers live.

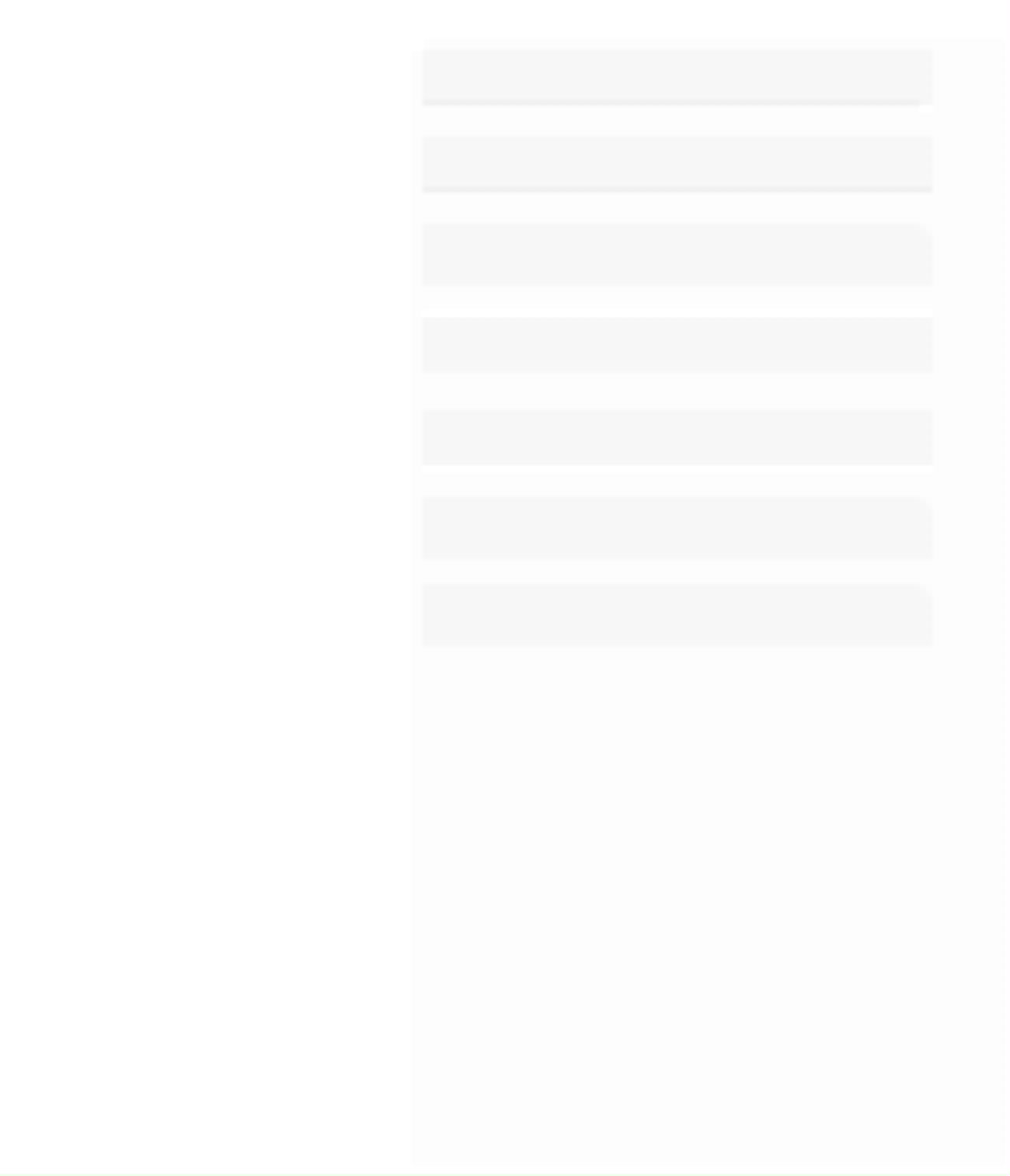

What will happen to the following types of private equity activity in the Benelux over the next 12 months?

Growth is expected for most PE categories

The survey results show that a large majority of respondents (82 percent) expect the number of add-on acquisitions to increase, indicating a strong trend toward smaller acquisitions to expand existing portfolios. In addition, 66 percent foresee an increase in platform acquisitions, indicating an increasing interest in acquiring companies that can serve as a basis for further growth.

63 percent also predict an increase in exits to strategic parties, with companies being taken over by strategic buyers. Furthermore, 51 percent see a growth in secondary buyouts, where companies are sold from one private equity party to another. In addition, 43 percent expect an increase in continuation funds, which support existing investments by holding funds longer.

“The continuation funds are likely to grow due to the difficulty in realizing exits and the need for liquidity solutions”, says Richard Reis, Partner at mid-cap investor Argos Wityu. “Secondary buyouts may see a slight increase as funds need for divestment and reinvestment, though I would approach this cautiously – it will be a very modest increase.”

It is striking that only 16 percent of respondents expect an increase in public-to-private deals (P2P), in which listed companies are withdrawn from the stock exchange, and almost a quarter even expect a decrease. “P2P deals are likely to decline as they add another layer of complexity to an already complex environment”, Reis explains.

Finally, only 35 percent foresee growth in venture capital investments, suggesting that this segment is less of a priority for investors.

A time to buy and a time to sell

There is money – 'dry powder' as it is called in M&A land – enough at many private equity firms. And according to many experts, it looks like they'll get it rolling in the coming months. At the same time, they have many companies and business units in their portfolio that they want to get rid of.

As Hans Swinnen, Partner at private equity firm 3d-investors, notes: "In private equity we see a trend where funds need to start divesting. Although this can be postponed for a year or two, it cannot be postponed much longer, especially as new funds are raised. We are already seeing more investors entering the market to sell. Confidence – or perhaps it is pressure – is increasing.”

“In private equity we are seeing a trend where funds need to start divesting. While this can be postponed for a year or two, it cannot be postponed much longer, especially as new funds are raised.”

Hans Swinnen, 3d-investors

There you have it: a basis for a flourishing market, with active private equity firms on the buying and selling sides. It may take a while before they assert themselves, says Véronique Gillis, Deals Partner at accounting and consultancy organization PwC Belgium: "For this they need a good economic climate. So I am still a bit cautious about the coming months, but quite optimistic afterwards."

Too many hunters, too little game

When asked about the biggest challenge for private equity in the Benelux, one answer clearly stands out, and it is on the buyer side: too many players chasing the same targets. 'Overcrowding' of the market, as Sander Neeteson, Head of Corporate Finance at ABN AMRO Bank, calls it.

What is the single biggest challenge private equity will face in thecoming 12 months in the Benelux?

This 'overcrowding' is encouraged by the fact that there are not always enough attractive 'targets' and because private equity parties are sometimes not selective enough.

“An unworkable situation”, says Tom Beltman, owner of mergers and acquisition specialist Marktlink. He advises private equity firms to specialize. An advice that is in line with the observation of Philippe Craninx, Managing Partner at mergers and acquisition specialist Moore Corporate Finance, that “private equity is often outbid by industrial buyers with greater sector knowledge and obvious synergy benefits.”

On the sell side, private equity firms also have their problems. An 'exit' is not always possible. Marcel Vlaar, Financial Due Diligence Partner at accounting and consultancy organization RSM Netherlands, sees this as the biggest challenge: "Exit opportunities are becoming scarce. This has to do with somewhat less current trading that the seller sees as temporary and that the buyer wants to price in."

"Exit opportunities are becoming scarce. This has to do with somewhat less current trading that the seller sees as temporary and that the buyer wants to price in."

Marcel Vlaar, RSM Netherlands

Marc Habermehl, M&A Lawyer-Partner at law firm Stibbe, agrees: "There are still relatively limited exit options at the moment. Finding the right exit is currently the primary concern for the investment community."

It is in line with what Sergio Herrera, Managing Director M&A at Rabobank says: "The biggest challenge will always be on the economic side. Weak economic growth is the most important challenge. This also affects the exit options." In other words, there is a risk that the 'good economic climate' that Véronique Gillis also talked about will take even longer to materialize.

So what should a PE firm that wants to sell do? Then a 'continuation fund' with partly new 'limited partners' might offer a solution, thinks Lieke van der Velden: "Selling at a low return is difficult. This could lead to an increase in transactions with continuation funds, in which companies are transferred to another fund managed by the same parties."

“However”, adds her colleague Joost den Engelsman, Head of Private Equity at NautaDutilh, “Private equity companies cannot put all their assets in continuation funds; they will have to bring attractive companies to the market. We are already preparing on a significant number of divestments in the first quarter or first half of 2025, and we expect other law firms to do the same.”

“Private equity companies cannot put all their assets in continuation funds; they will have to bring attractive companies to the market.”

Joost den Engelsman, NautaDutilh

Conclusion: Good timing and substantive knowledge are even more important

Many more add-ons by private equity firms: that is the main expected development in the coming 12 months. More generally: their willingness to invest appears to be increasing. In order to compete with other investors, (further) specialization may be a good idea.

At the same time, the pressure to sell is also increasing. However, an exit is not always easy. Little is expected at all from 'public-to-private deals'. Other exit options are more promising. Sales to strategic parties are mentioned most often by the dealmakers who participated in this study. Otherwise, a continuation fund might offer a solution. This is an option that is also used to retain the best assets for longer. For example, the successful Action retail chain has been in 3i's portfolio since 2006 and has been rolled over several times into a new structure.

Share this article